The IRS is currently in the process of issuing Notices CP508C to hundreds of thousands of U.S. taxpayers—placing all notified taxpayers’ passports in serious jeopardy. Several news outlets this week report that the U.S. State Department confirms that it has already acted on its part in the process and denied passports to an undisclosed number of taxpayers. Reports also confirm that the IRS has already successfully collected over $11.5 million from over 200 taxpayers trying desperately to avoid passport denial. Passport denials are alarming enough—but the same authority used to deny passports also grants the IRS and the U.S. State Department the power to work in tandem to revoke a passport, as well. Concerned taxpayers should not wait to travel abroad before carefully considering their circumstances.

Who’s at Risk?

Enacted in 2015, the Fixing America’s Surface Transportation Act (FAST Act) provided that the State Department must deny a passport application by any individual certified by the IRS as having a “seriously delinquent tax debt.” Additionally, the FAST Act authorizes the State Department to revoke a passport held by an individual with seriously delinquent tax debt. The certification process itself is governed by Internal Revenue Code (I.R.C.) §7345, which also provides taxpayers a limited right to judicial review.

Again, a taxpayer is at risk of passport denial or revocation if they are certified as having “seriously delinquent tax debt.” The elements of a “seriously delinquent tax debt,” are as follows:

- It is an unpaid, legally enforceable federal tax liability of an individual.

- The liability must be assessed.

- The liability must exceed $50,000.

- The IRS must have filed a notice of federal tax lien under I.R.C. §6323, or levied under §6331 with respect to the liability.

On the other hand, under I.R.C. §7345(b)(2), “seriously delinquent tax debt” does not include: (1) a liability being paid timely pursuant to an installment agreement or an offer-in-compromise, and (2) a liability for which a collection due process (CDP) hearing or innocent spouse relief request is pending. Besides these statutory exceptions the IRS currently exercises discretion, subject to change, to exclude additional categories of liability listed in Internal Revenue Manual (I.R.M.) sections 5.1.12.27.4 (12-20-2017) and 5.19.1.5.19.4. These categories include:

- Debt that is currently not collectible (CNC) due to hardship

- Debt that resulted from identity theft

- Debt of a taxpayer in bankruptcy

- Debt of a deceased taxpayer

- Debt that is included in a pending Offer in Compromise

- Debt that is included in a pending installment agreement

- Debt of taxpayers in a Disaster Zone

- Debt with a pending adjustment that will full pay the tax period

The Certification Process

Until recently, the mechanics of the certification process, and any potential for reversal of it, were rather obscure. On April 5, 2018, the Chief Counsel’s Office provided advice in Notice CC-2018-005 to Chief Counsel attorneys who handle I.R.C. §7345 passport actions. The Notice shed light on the matter, detailing both the certification and reversal processes for “seriously delinquent taxpayers,” as well as the procedures for the judicial review of certifications.

Per Notice CC-2018-005, it is clear that the IRS is relying “on automated systems to identify every module (electronic record of tax liability) on an individual’s account with an unpaid assessed tax liability that is not statutorily excepted from the definition of seriously delinquent tax debt or otherwise in a category excluded from certification.” Once identified, according to the Notice, the systems will total the amount of unpaid liabilities; if the resulting total exceeds the statutory threshold, then the taxpayer will be identified as having a seriously delinquent tax debt. The Notice clarifies that under these circumstances, a Transaction Code (TC) 971 Action Code (AC) 641 will then post to each module.

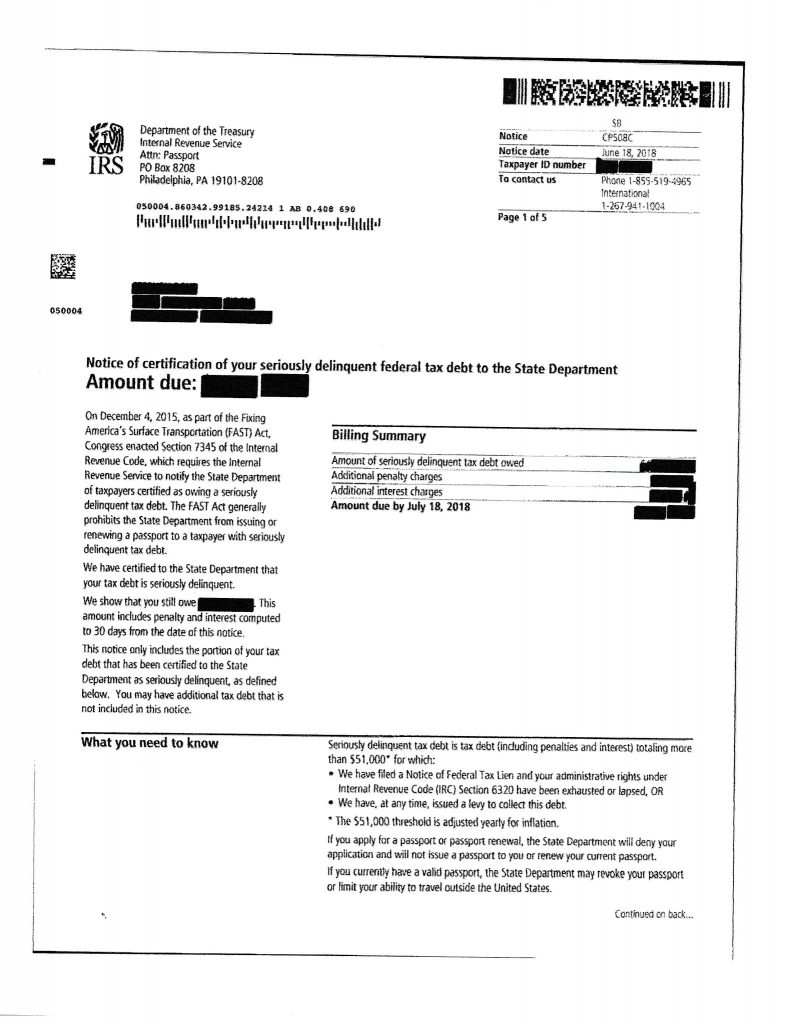

The next part of the process, according to the Notice CC-2018-005, is that the Small Business/Self Employed Commissioner will make the certification, and the IRS will provide the list of all certified individuals to the State Department. Upon receipt of this list, the State Department will not issue a passport to a listed individual, and it may revoke an already-issued passport, except as necessary for return travel to the United States. Notice CC-2018-005 also states that along with the certification, the IRS will notify individuals of their certification by issuing them Notice CP508C by regular mail. Among other things, the Notice CP508C will inform the individual of the right to judicial review in a federal district court or the Tax Court. Many taxpayers have already received the Notice CP508C, a sample of which is attached herein.

Certification Reversal

Reversing the certification is required under three circumstances. I.R.C. §7345(c) requires reversal of certification when:

- Certification is found to be erroneous,

- The seriously delinquent tax debt is fully satisfied, or

- The debt ceases to be a seriously delinquent tax debt due to an exception under I.R.C. §7345(b)(2).

Additionally, according to Notice CC-2018-005, certification reversal will also result when the debt falls into one of the discretionary exclusion categories listed in IRM sections 5.1.12.27.4 and 5.19.1.5.19.4. “either entirely or in combination with the circumstances listed in section 7345(c), or the taxpayer enters a combat zone or participates in a contingency operation within the meaning of section 7508(a).”

Once a certified module is qualified for reversal, a TC 972 AC 641 will be posted to it, according to Notice CC-2018-005. Certification “will not be reversed until all modules covered by it have been fully satisfied or otherwise meet the criteria for reversal,” the Notice clarifies. After the TC 972 AC 641 is posted, the IRS will concurrently provide notice of the reversal to both the taxpayer and the State Department. The taxpayer will be notified in a CP508R Notice by regular mail.

Guidance re Judicial Review of Certifications

Any certified individual may bring a civil action to determine the validity of the certification or whether the certification should have been reversed. Such action may be filed in either a federal district court or against the Commissioner in the Tax Court. Note that if an action is filed in both federal district court and the Tax Court, the court where the first action was filed has sole jurisdiction. Furthermore, if the court finds an erroneous certification, or that certification should be reversed, the court may order the IRS to notify the State Department.

Additionally, Notice CC-2018-005 states that the Tax Court has proposed adding a new Title XXXIV to its Rules of Practice and Procedure. Generally, the proposed rules would:

- Describe the court’s jurisdiction,

- Specify the title and content of a petition,

- Require the filing of an answer, and

- State when the case is deemed at issue.

The proposed rules would also require, according to Notice CC-2018-005, that a petition include a copy of the CP508C Notice.

Notice CC-2018-005 further identifies and discusses three issues that are expected to be raised by petitioners in certification challenges (ones that the Code fails to specifically address). Specifically, it anticipates challenges to the underlying liabilities, the statute of limitations for bringing an action, and the scope and standard of review.

First, Notice CC-2018-005 emphasizes that judicial review under I.R.C. §7345 does not include review of the amount of the liability. Secondly, since I.R.C. §7345(e) lacks a specific period of limitations within which a certification action may be brought, the Notice explains that a period of six-years will apply. Thus, individuals will have six years from the issuance of a certification notice to bring an action. Finally, as I.R.C. §7345(e) also fails to specify the scope or standard of review for certification actions, the Notice cites 5 U.S.C. §706(2)(A) in that “review should be limited to the Service’s records and whether the certification or failure to reverse the certification was ‘arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with law.” Significantly, the Notice advises that for certification actions arising in Tax Court, I.R.C §7482(b)(1) places appellate venue in the U.S. Court of Appeals for the District of Columbia Circuit.

Be Proactive

Taxpayers with “seriously delinquent tax debt” and wishing to maintain their passport privileges are well advised to consult with a tax professional for reaching an arrangement with the IRS to prevent certification or achieve reversal of an existing certification.